Most people start a company to build a product, serve their community, or solve a specific problem. Very few people start a business because they love staring at spreadsheets. Yet keeping track of every dollar quickly becomes a demanding second job for almost every founder.

Closing the books at the end of the month usually involves late nights, lost receipts, and the nagging feeling that your numbers might be completely wrong. Historically, keeping financial records has been a massive manual chore. But the environment of small business accounting has shifted entirely over the last few years.

Smart software and artificial intelligence have entered the finance space in a big way. This is not the science fiction version of robots taking over the world. The reality of automated reporting is incredibly practical. It simply handles the boring stuff. It catches the silly mistakes we all make and gives business owners a clear view of their cash. At MagicBooks, we help founders modernize these daily money tasks. We see exactly how getting the numbers right changes the way a business operates on a fundamental level.

Here is a simple look at how automated systems are changing the monthly reporting process, why it actually matters for your bottom line, and how to use it without losing control of your business.

What Automation Actually Means for Your Money

When people hear about artificial intelligence in business, they usually picture complex algorithms that require a computer science degree to understand. In the context of your business finances, the reality is much simpler. It refers to software that can recognize patterns, learn from your previous actions, and handle repetitive tasks without needing you to click every single button.

To really understand the shift, you have to look at the difference between traditional bookkeeping and modern automated reporting.

Traditional accounting software is essentially a digital filing cabinet. If you buy printer ink, you have to log into your system. You have to type in the name of the store. You have to enter the date and the exact amount. Then you have to select the correct expense category from a long list. The software does nothing on its own. It only knows exactly what you tell it.

Modern bookkeeping actively works alongside you. When a charge from an office supply store hits your bank feed, the system looks at the vendor name. It remembers how you categorized similar expenses two months ago and fills in the blanks for you.

Your accounting system moves from being a passive storage folder to an active participant in your daily operations.

Fixing the Worst Parts of the Monthly Close

So what does this look like on a random Tuesday when you are trying to get your accounts in order? Smart systems tend to shine in a few highly specific areas of the monthly workflow. These are usually the tasks that business owners hate doing the most.

Making Manual Data Entry Disappear

Typing numbers into a computer is slow and incredibly prone to mistakes. It is very easy to accidentally type $45.90 when the receipt actually says $49.50. This might sound like a tiny mistake, but a small typo can throw off your entire balance sheet. For a deeper look at how simple mistakes cause massive headaches when balancing your books, check out this guide on the transposition error.

Automated data entry tools scan your invoices and pull the relevant numbers immediately. They drop those numbers right into your general ledger. This drastically reduces the typos that ruin your weekend when you are trying to close the books.

Speeding Up Bank Reconciliation

Bank reconciliation is the process of matching the money leaving and entering your actual bank account with the records in your software. Anyone who has run a business knows this is often the most tedious part of the month. You sit there trying to match a random $200 charge on your bank statement with a pile of paper receipts.

Newer software speeds this up by instantly matching bank feed lines to invoices. Instead of hunting for the matching receipt, the software suggests the match automatically. You just have to review it and click to confirm.

Spotting Anomalies and Catching Mistakes

Humans get tired. When you are reviewing hundreds of expenses on a screen, your eyes naturally glaze over. You might not notice that your monthly internet bill was suddenly billed at double the normal rate.

Software does not get tired. It constantly scans your financial data for things that look weird. If a vendor accidentally charges your card twice, or if an expense falls wildly outside your normal spending patterns, the system will flag it. You get a notification to review the charge before it ends up permanently logged in your ledger.

Moving From Historical Records to Future Planning

One of the biggest problems with manual bookkeeping is that it is always backward-looking. By the time you finish gathering your receipts, matching your bank accounts, and building your spreadsheets, it is already the middle of the following month. You are looking at a historical snapshot of money you have already spent.

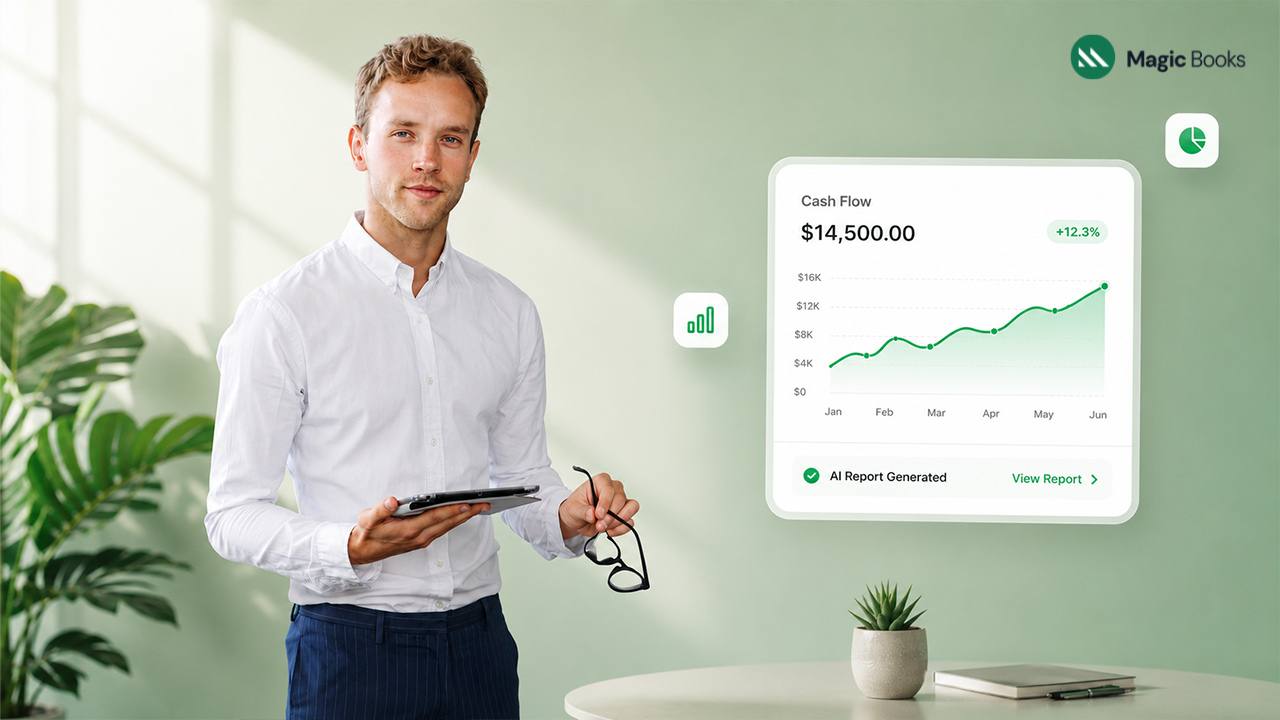

Automated tools help shift your focus from a historical record to a forward-looking strategy. Because data entry and categorization happen almost in real time, your books are constantly up to date.

This speed unlocks something crucial for small businesses. It unlocks forecasting.

A modern financial tool can look at your cash flow history, your upcoming bills, and your average incoming revenue to predict where your bank balance will be in three weeks. You no longer have to guess if you can afford to buy new equipment or hire some extra help for the busy season.

A platform like MagicBooks handles the tedious backend categorization so you can focus on these bigger questions. When your baseline data is organized accurately, generating your monthly financial reports becomes a fast process rather than a stressful project. You get faster answers, and faster answers lead to better business decisions.

How the Role of Your Bookkeeper Changes

A very common worry among business owners is that relying on automation means they are flying blind. They worry that using smart software will replace the human expertise they desperately need to stay compliant with tax laws.

The reality is quite the opposite. These tools are not replacing accountants or bookkeepers. Instead, they are changing their job description for the better.

Think about it logically. When a professional bookkeeper does not have to spend ten hours a month manually typing in your receipts, they gain ten hours of free time. They can spend those ten hours actually analyzing your business model. They can help you figure out why your profit margins are shrinking on a specific product line. They can advise you on tax strategies before the end of the year approaches. The relationship moves from simple data entry to valuable financial advising.

If you are wondering how this dynamic works in practice, this connects with knowing the signs it is time to hire a bookkeeper. Even with the smartest software in the world, having a human expert review your finances provides a layer of critical thinking that an algorithm simply cannot offer.

For related reading on getting expert help to manage your growing financial needs, you might explore the benefits of outsourcing your accounting needs. Alternatively, if you are confused about the different types of financial professionals out there, reading up on the CPA vs EA difference can help you figure out exactly who you need in your corner.

Knowing the Limits and the Real Risks

As helpful as all this technology is, you have to stay grounded. Automated reporting is a fantastic tool, but it is not magic. It has real limitations that small business owners absolutely need to understand to avoid getting into trouble with the IRS or their investors.

The biggest risk by far is the classic “garbage in, garbage out” problem. Automated systems rely entirely on the data they receive. If you have a bad habit of mixing your personal and business expenses on a single credit card, the software will struggle. It might confidently categorize your personal grocery shopping as a business office supply expense. If you do not catch that mistake, your profit and loss statement will be entirely wrong. This will cause massive issues and potential penalties come tax season.

Overreliance is another major trap. It is very tempting to let the software run on autopilot and never look at the actual ledger. You might assume the computer is always right. But automatic categorizations are really just educated guesses based on past behavior. Sometimes a monthly software subscription might be categorized as an advertising expense when it really should be an IT expense.

You still need a human to review the final output. You cannot just close your eyes and trust the machine blindly.

This is exactly why setting up routine checks is so vital to your success. If you find that your automated reports are occasionally looking strange, you have to dig in and find the root cause. This connects perfectly with knowing when you should conduct an internal audit in your business. Running a simple internal audit helps you catch these systemic hiccups early. It allows you to retrain the software to categorize things correctly moving forward.

Why Clearer Reporting Actually Matters

At the end of the day, nobody implements new financial technology just for the fun of it. Learning new software takes time and effort. You do it because poor financial reporting is a silent killer for small companies.

When your reporting is slow and messy, you are forced to make decisions based on gut feelings rather than hard facts. You might spend money you do not actually have. On the flip side, you might hold back on a great growth opportunity because you falsely believe your cash is too tight.

By automating the tedious busywork, you gain clear and highly accurate visibility into the health of your business. With up to date numbers at your fingertips, it becomes much easier to track the financial ratios a small business owner should know. You can easily check your current ratio or your gross profit margins on any given day. You move from running your business in the dark to operating with the lights turned all the way up.

Wrapping It Up

Financial reporting really should not be the hardest part of running your business. The introduction of smart software into small business accounting means that the days of painful data entry, endless bank reconciliations, and broken spreadsheets are slowly coming to an end.

By letting software handle the repetitive and error prone tasks, you get your time back. You get faster access to your monthly reports. Most importantly, you gain the confidence to make better financial decisions for the future of your company. You absolutely still need human oversight, and you still need to understand your own numbers, but the heavy lifting is finally being taken off your shoulders.If you are looking for a practical way to get your finances in order without pulling your hair out, MagicBooks offers a straightforward solution. It is built specifically to keep your data organized, make your reporting crystal clear, and ensure your business is ready for whatever comes next.