When one hears the phrase “cost accounting”, the first thing that may come to mind is an uneventful routine that is often carried out after all the business activities have been performed. However, in practical terms, it is the most critical element of business decision making. Call it the navigation system that you require to take you through any difficult business terrain. Otherwise, you could be in a situation where you are hopping from one customer to another trying to figure out if your prices are enough to cover all of your costs or if there are certain projects that are quietly draining all of the resources into a bottomless pit.

Now suppose that in every spending decision you have made there is a single explanation attributed to each single dollar and not just a figure in a generalized ledger But information which shows what price to charge, what resources to use, where you need to bring in efficiencies and as a last result improve your profits.

Cost accounting is more than just a tool for accountants; it can also help business owners and managers drive development, increase efficiency, and make better informed, strategic decisions. And, guess what? If you operate a B2B business, cost accounting is your hidden weapon.

What Is Cost Accounting?

Cost accounting is a managerial accounting process that captures a company’s costs of production by evaluating the input costs of each stage of production as well as fixed costs, variable costs, and overhead. Unlike financial accounting, which is mainly used for external reporting, cost accounting is focused on the internal processes in business decisions.

Why Is Cost Accounting Important for B2B Companies?

The benefits of cost accounting for B2B companies are quite profound and multifaceted:

- Rises Profitability: Determination of costs of products or services allows businesses to charge at levels that will guarantee them profit and yet remain competitive.

For example, a manufacturing firm using cost accounting can easily calculate the total production cost for a given product. From this, they will be able to set a selling price that ensures cost coverage but also contributes to its profit margins. - Facilitates Strategic Planning: It is useful in making long-term strategic plans as well as allocation of resources.

The example: A consulting business might compare the expenses of one service it offers to another in order to ascertain which one would optimize its profit margins and allow it to concentrate marketing efforts in the most lucrative regions. - Helps in Increasing Operational Efficiency: Companies identify instances of waste and operating inefficiency. This helps to streamline operations as well as reduce costs.

For example, a company that wants to save money and time on development of pricey software might utilize cost accounting to understand the requirements for implementing effective coding practices. - Oversees Budgeting and Forecasting: Reasonable budgets and forecasts, which are essentially crucial determinants of financial health, need the development of trustworthy cost information.

For example, a logistics business can use past cost data for its projections of future costs and thus determine an annual budget that guards against periodic fluctuations in demand.

Key Concepts in Cost Accounting

Understanding cost accounting involves familiarizing yourself with several key concepts that are foundational to effective cost management.

Direct Costs vs. Indirect Costs

- Direct Costs: These are expenses that can be directly traced to a specific product or service. They include raw materials and labor costs associated with production.

- Indirect Costs: These are costs that cannot be traced directly to a single product or service. Instead, they are shared across multiple products or services and include overhead expenses like rent and utilities.

| Type | Definition | Example |

| Direct Costs | Expenses directly tied to production or service. | Raw materials for machinery; labor for project. |

| Indirect Costs | Shared expenses not tied to specific products. | Rent; utilities; salaries of administrative staff. |

Fixed Costs vs. Variable Costs

- Fixed Costs: These costs remain constant regardless of production levels, such as rent or salaries.

- Variable Costs: These costs vary based on the level of production. For example, raw materials increase as more units are produced.

| Type | Definition | Example |

| Fixed Costs | Costs that do not change with production volume. | Monthly lease for office space. |

| Variable Costs | Costs that fluctuate based on production levels. | Costs of raw materials used in production. |

Overhead Costs

Overhead costs are necessary for running a business but cannot be directly attributed to a specific product. These include utilities, rent, and salaries for non-production staff. Understanding overhead is crucial for accurate cost allocation.

Cost Allocation

Cost allocation is the process of assigning indirect costs to different departments, products, or services based on specific criteria. This helps in understanding the true cost and profitability of each segment of the business.

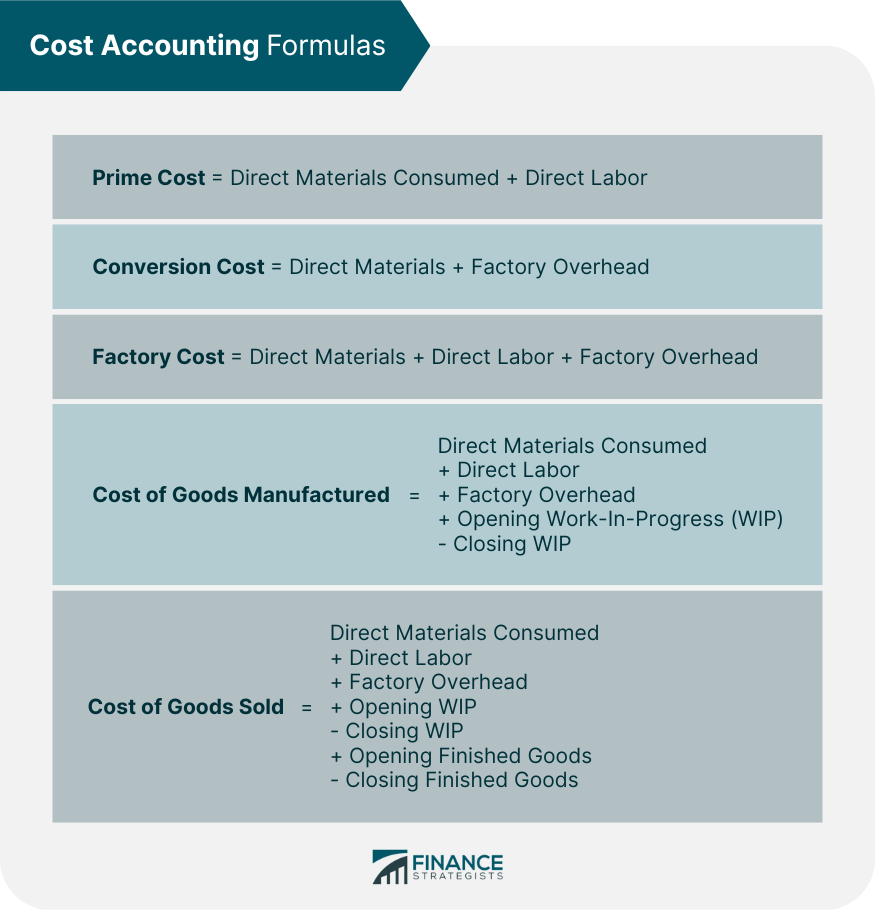

Source: Cost Accounting Formulas | Formula, Calculation, and Example

Methods of Cost Accounting

Different methods can be employed to track and analyze costs, each suitable for different types of businesses and industries. Here are some common methods:

- Job Order Costing

For companies that offer customized goods or services, job order costing is perfect. Because costs are monitored for every single work or project, figuring out profitability on a job-by-job basis is made simpler.

Example: To keep track of the expenses related to each piece of bespoke furniture they make, a manufacturer employs work order costing. This covers the price of labor, wood, and any additional supplies needed. They are able to precisely determine the cost of each item by using this method.

- Process Costing

Process pricing works well for businesses that make a lot of identical items. This approach is perfect for continuous manufacturing operations since costs are averaged over the number of units produced.

For instance, Process costing is used, for instance, by a food processing facility to calculate the cost per unit of its packaged items. The factory can determine competitive prices for its goods by dividing the entire expenses incurred during a production period by the total number of units produced.

- Activity-Based Costing (ABC)

Activity-based costing (ABC) breaks down costs by the specific tasks that have an impact on expenses giving a more accurate view of the prices linked to different products or services. This approach works well for complex companies that offer a wide range of items.

Take a logistics firm as an example. It might use ABC to figure out the costs to process orders, run warehouses, and ship packages. By keeping track of the expenses tied to each task, the company can spot which services make the most money and tweak its pricing plan.

- Standard Costing

Standard costing sets up fixed prices for goods and services, which people then compare to actual costs. This method helps companies spot differences and keep expenses in check more.

Let’s say a factory comes up with set prices for each part of a product. By looking at real costs next to these benchmarks, the company can find out where they’re spending more than they planned and fix the problem.

Implementing Cost Accounting:

Integrating cost accounting into your business may seem daunting, but by following these structured steps, you can create an effective cost accounting system.

Step 1: Identify Costs

Start by identifying all costs associated with your products or services. Break them down into categories such as direct costs, indirect costs, fixed costs, variable costs, and overhead costs.

Example: A construction company might categorize its costs as follows:

| Cost Category | Direct Costs | Indirect Costs |

| Labor | Wages of construction workers | Administrative salaries |

| Materials | Concrete, steel, lumber | Office supplies |

| Overhead | N/A | Rent, utilities, insurance |

Step 2: Choose a Costing Method

Select the most appropriate costing method based on your business model. Consider the nature of your products or services and industry standards.

Example: A service-based company might choose job order costing to track the costs of individual projects, while a manufacturing firm may opt for process costing.

Step 3: Gather Data

Collect data related to costs, including invoices, payroll records, and expense reports. Ensure that the data is accurate and up-to-date, as this is crucial for effective cost accounting.

Example: A tech startup can use accounting software to automate the collection of expense data from various departments, ensuring that all costs are captured in real time.

Step 4: Analyze Costs

Once you have collected the necessary data, use it to analyze costs. Look for trends, variances, and areas for improvement. This analysis will provide valuable insights into your business operations.

Example: A marketing agency might analyze its campaign costs to determine which types of campaigns generate the highest returns. This analysis could lead to a shift in focus toward the most profitable services.

Step 5: Make Informed Decisions

Utilize insights from your cost analysis to make informed decisions regarding pricing, budgeting, and resource allocation.

Example: A SaaS company might determine that a specific feature is driving significant revenue. Based on this analysis, the company can allocate more resources to developing and marketing that feature.

Step 6: Monitor and Adjust

Cost accounting is an ongoing process. Regularly monitor your costs and adjust your strategies as needed. This approach ensures that you remain agile in responding to market changes.

Example: A logistics company continually reviews its delivery costs and adjusts routes and carriers based on fluctuating fuel prices and customer demands.

Challenges of Cost Accounting

While cost accounting is invaluable for B2B businesses, it is not without its challenges. Here are some common hurdles companies may face:

- Data Accuracy: Inaccurate data can lead to flawed cost calculations and poor decision-making. Implementing robust data collection processes is crucial.

- Complexity of Allocation: Allocating indirect costs can be complex and subjective, making it challenging to determine accurate costs for products or services.

- Changing Costs: Fluctuating costs, such as raw materials and labor, can make it difficult to maintain accurate cost projections.

- Resistance to Change: Employees may resist adopting new cost accounting practices, especially if they perceive them as additional work.

Overcoming Challenges

To overcome these challenges, consider the following strategies:

- Invest in Training: Train personnel on cost accounting concepts and procedures. This will guarantee that everyone knows the significance of precise data collecting.

- Utilize technology: Use accounting software to automate data gathering and analysis, decreasing staff workload and increasing accuracy.

- Foster a Culture of Transparency: Encourage open discussion regarding expenses and their implications for the firm. This can assist to reduce opposition to new methods.

Conclusion

You have now learned how cost accounting power can go beyond tracking expenses, in fact, it can be a means of finding greater profitability, efficiency, and growth. It is not about cranking numbers but having a better view of how your business operates and using that view for smarter decisions.

Business enterprises that do not understand their costs are, most often, scrambling trying to figure out where the profits are disappearing. Business enterprises embracing cost accounting, though? They’re the ones thriving, able to make decisions with a great deal of confidence and staying well ahead of the curve.

And so the next time you have to make a huge decision over whether it’s setting prices, new investments in technology, or expanded operations remember the power of cost accounting. It’s your roadmap to success-someone takes you through the maze of complexity that comes with having a business of your own-clear and direct.

Your turn: Now you put cost accounting to work. Begin by analyzing your current projects, tracing out costs, and starting to make improvements. Over time, such insights compound and drive your business forward.