An organization’s success depends on knowing how much working capital it has available to pay payments when they become due. A solid balance sheet is not always the outcome of concentrating solely on earnings. It’s business efficiency through working capital that everyone needs to understand, and automatic replenishment of stock does help, but with working capital management. Overhead working capital is also an important aspect to highlight because an overdeveloped part of the capital can cause enormous pressure on the business operation. On the other hand, when a company is looking for a clearer structure of its balance sheet, i.e., what would be the maximum possible amount an investor would have to put into the company, it is essential to add working capital guides to what will be included within the debt section of the capital structure schema. In this manner, it is vital to understand how working capital influences loan repayments and which parts of the debt burden the company. So, what exactly did I mean when I said working capital formula? Please see further the article/conversation.

Working capital can be described as a financial measure that is used to determine the residual balance of a company’s assets and liabilities. Reconciling with working capital as a financial measure assists in planning future needs while also ensuring that the company has adequate liquid or near-liquid assets to meet its outstanding debt and short-term loans repayable within the year.

A company can have negative working capital or positive working capital.

Positive working capital: This implies that when the amount is positive, it can be said that the current assets of a company are greater than the current liabilities, as depicted in the above example. This situation means that the company can cover its short-term loans and also maintain some bonus cash in situations where all short-term assets are used up to offset those loans.

Negative working capital: When the amount is negative, it means that the current liabilities outweigh the firm’s current assets. This raises a red flag about the firms’ short-term debts which are making the firm depleted of short-term assets. It tends to indicate the existence of negative short-term conditions, poor liquidity, and future problems settling debt maturities.

What are the Constituents of Working Capital?

Working capital consists of current assets and current liabilities.

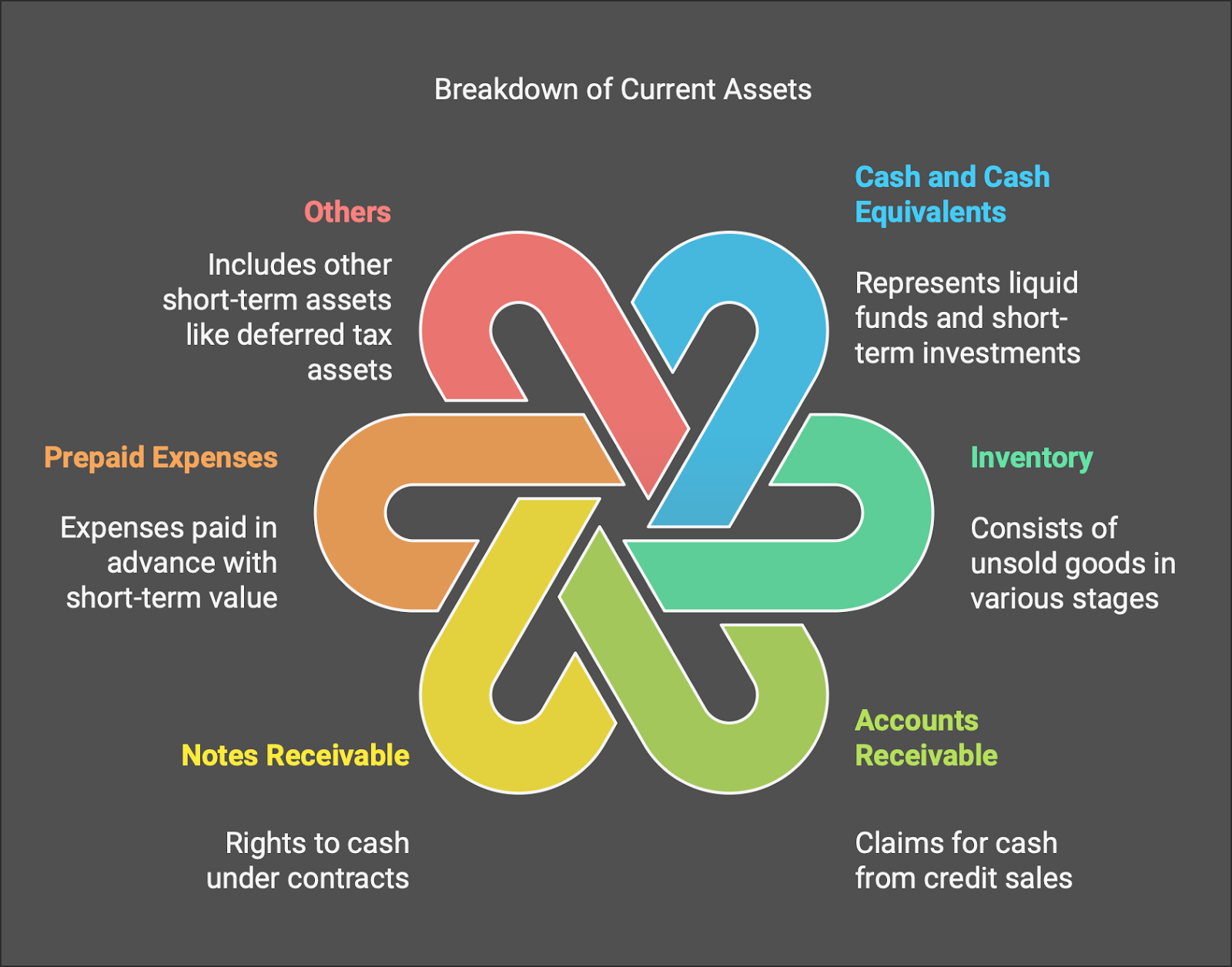

Current Assets ➝ Current assets are supposed to be turned into cash within twelve months or one year, which is the time considered the standard operating cycle.

- Cash and cash equivalents: All the company’s money on hand, including foreign investments and low-risk, short-term investments like money market accounts.

- Inventory: Unsold goods, which may be raw materials, work-in-progress, or finished goods not yet sold.

- Accounts receivable: Claims to cash for items sold on credit, net of any allowance for doubtful payments.

- Notes receivable: Rights to cash under other contracts, typically evidenced by a signed agreement

- Prepaid expenses: The value for expenses paid in advance, which, although difficult to liquidate, still have a short-term value.

- Others: Any other short-term asset. For example, some companies may have a short-term deferred tax asset that offsets a future liability.

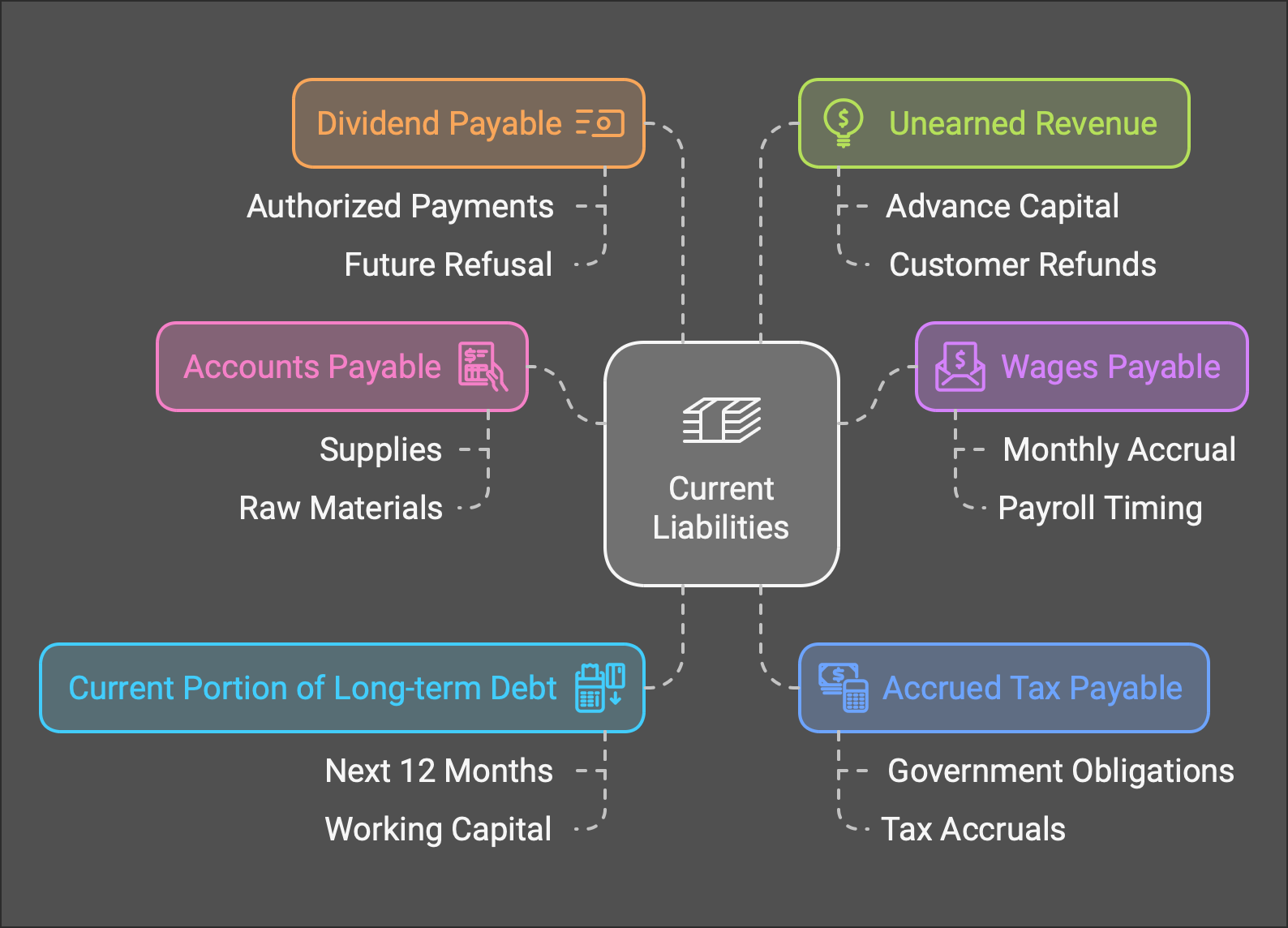

Current Liabilities ➝ Similarly, current liabilities are expected to be paid within a firm’s twelve months.

- Accounts payable: Unpaid invoices due vendors for supplies, raw materials, utilities, property taxes, rent, or any other operating expense owed. Usually, credit terms on invoices are 30 days, capturing almost all the invoices.

- Wages payable: The amount of unpaid salaries and wages for employees. This usually accrues up to one month’s worth of wages, depending on the timing of the payroll.

- Current portion of long-term debt: Short-term payments related to long-term debt. Only the next 12 months’ payments are included in working capital calculations.

- Accrued tax payable: Obligations to government bodies, including accruals for tax obligations not due for months but payable within the next 12 months.

- Dividend payable: Payments authorized to shareholders. Although a company may refuse future dividend payments, it does have to pay dividends authorized previously.

- Unearned revenue: Capital received in advance of performing work. If the firm does not finish the job, it may have to return this capital to the customer.

How to determine working capital

The working capital of the organization can be calculated from the resources employed by the organization in the form of current assets, which include cash, account receivables, inventories, marketable securities, and other similar assets minus the liabilities that are due within the financial period.

Current liabilities are operational expenses such as rent, accrued expenses, and accounts payable that must be settled within the year.

The equation can, therefore be summarized as follows:

Working Capital = Current Assets – Current Liabilities

Working Capital Ratio Formula

The working capital ratio looks like a fraction that contributes to the ratio and understanding of the financial position of a company, its current assets divided by current liabilities, where the working capital ratio is regarded as one of the liquidity ratios.

The working capital ratio is computed by taking the current assets over the current liabilities.

Working Capital Ratio = Current Assets ÷ Current Liabilities

Where ;

Positive Working Capital Ratio ➝ In the case where a business has a working capital ratio of greater than 1.0x, it implies that the business has a positive working capital.

Negative Working Capital Ratio ➝ On the other hand, if the working capital ratio is less than 1.0x, then a company has an aggregate working capital deficiency.

How to Calculate Working Capital Ratio

One standard financial ratio used to measure working capital is the current ratio, a metric designed to provide a measure of a company’s liquidity risk.

The current ratio is computed as a company’s current assets divided by its current liabilities.

Current Ratio = Current Assets ÷ Current Liabilities

The current ratio is of limited utility without context. Still, a general rule of thumb is that a current ratio of > 1.0x implies that a company is more liquid because it has liquid assets that can presumably be converted into cash and will more than cover the upcoming short-term liabilities.

The quick ratio—or “acid test ratio”—is a closely related metric that isolates only the most liquid assets, such as cash and receivables, to gauge liquidity risk.

Why? The advantage of ignoring inventory and other non-current assets is that liquidating inventory may not be easy or advisable, so the quick ratio excludes those as a source of short-term liquidity.

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable) ÷ Current Liabilities

Compared to the current ratio, the quick ratio is viewed as the more conservative measure of liquidity, considering only cash and

What Is Working Capital Management?

It’s akin to performing a circus act when one talks about working capital management. Capital management involves a business’s requirement to not only ensure that it does not have a deterring backhand, but even so, it begins to overhead as well, is somewhat rotten. But in reality, if done correctly, it permits all the bills to be paid, all the cash registers to be operational, and all the aspects of a person’s business to function without issue.

Some financial ratios can easily overarch this entire circus act. Let’s list them.

- Working Capital Ratio: You might say that this helps to keep a check on the growth plans of the company and its other working factors. This shows a business’s resource level in relation to unpaid obligations within a specific time frame. Formally, it is expressed as total current assets over total current liabilities.

- Average Collection Period: This checks how quickly you get paid for credit sales. Shorter collection periods mean cash is flowing well; longer ones mean you’re essentially giving out free loans. To calculate, divide the average accounts receivable by total net credit sales and multiply by the number of days in the period.

- Inventory Turnover Ratio: Here is the ratio for your stockpile. Are you selling inventory quickly, or is it gathering dust? Higher turnover means you are moving products efficiently, while low turnover could suggest it is time to have a clearance sale. The formula? Cost of Goods Sold (COGS) divided by average inventory value.

Why working capital is important?

Working capital (WC) is important for keeping a business afloat. In particular, keeping money in and out of the business is vital.

A larger financial buffer lets a company manage excessive debt better, fulfill financial duties, and maintain a stable environment. All of these keep employees and investors happy.

And the more this liquidity buffer builds, the better positioned the company will be to grow.

When such funds are low or negative—meaning liabilities are higher than assets—this could mean that a company might find it challenging to settle short-term liabilities and is more prone to setbacks without additional financing.

It’s also possible for working capital to be too high. Very high levels indicate that the company isn’t investing wisely and letting too much money sit idle.

It should be remembered that the optimal level of liquidity varies depending on the nature of a business or industry. What works for one company might not work for another, and low or negative operational capital doesn’t always mean a company is in trouble.

Ways to increase Working Capital Effortlessly

The first thing that comes to our mind is the uncertainty that hits small businessmen during their cash flow. Their projects get so busy that they may lose their focus, or their sales may drop down like never before. There are synonyms, so there is no need to worry! Here we are with some creative tricks that will help you make working capital stronger:

- Leverage Long-Term Loans: By Increasing cash resources and at the same time avoiding the accumulation of short-term debt. This alone gives the most essential cash boost to a business without the consequences.

- Extend The Payment Terms: While this sounds loopy enough if you simply keep your eyes on your cash flow, the answer is not cash flow forecasting; it is out of cash flow: It eliminates all the scariness of payables.

- Liquidate Non-Core Assets: If there were ever assets or things that deserve a sooner or later status, your list has most likely just gotten longer. Take that cash and use it. Additionally, you may enhance your Kondo-ing efforts.

- Restrict Costs: If everything goes according to the plan, the number of payables has dropped and significantly more headspace is available. Dive deep into those cash flows and split them right.

- Improve Inventory Turnover Ratio: Too much money tied up in inventory is stock puffed out free cash. Maintain an adequate inventory level, and make sure you don’t overstock where you don’t have to.

- Implement Receipt and Payment Automation: Today’s solutions are far more than cool; they are worth the hype. Take advantage of automating your incoming and outgoing cash, and your working capital troubles will be a thing of the past.